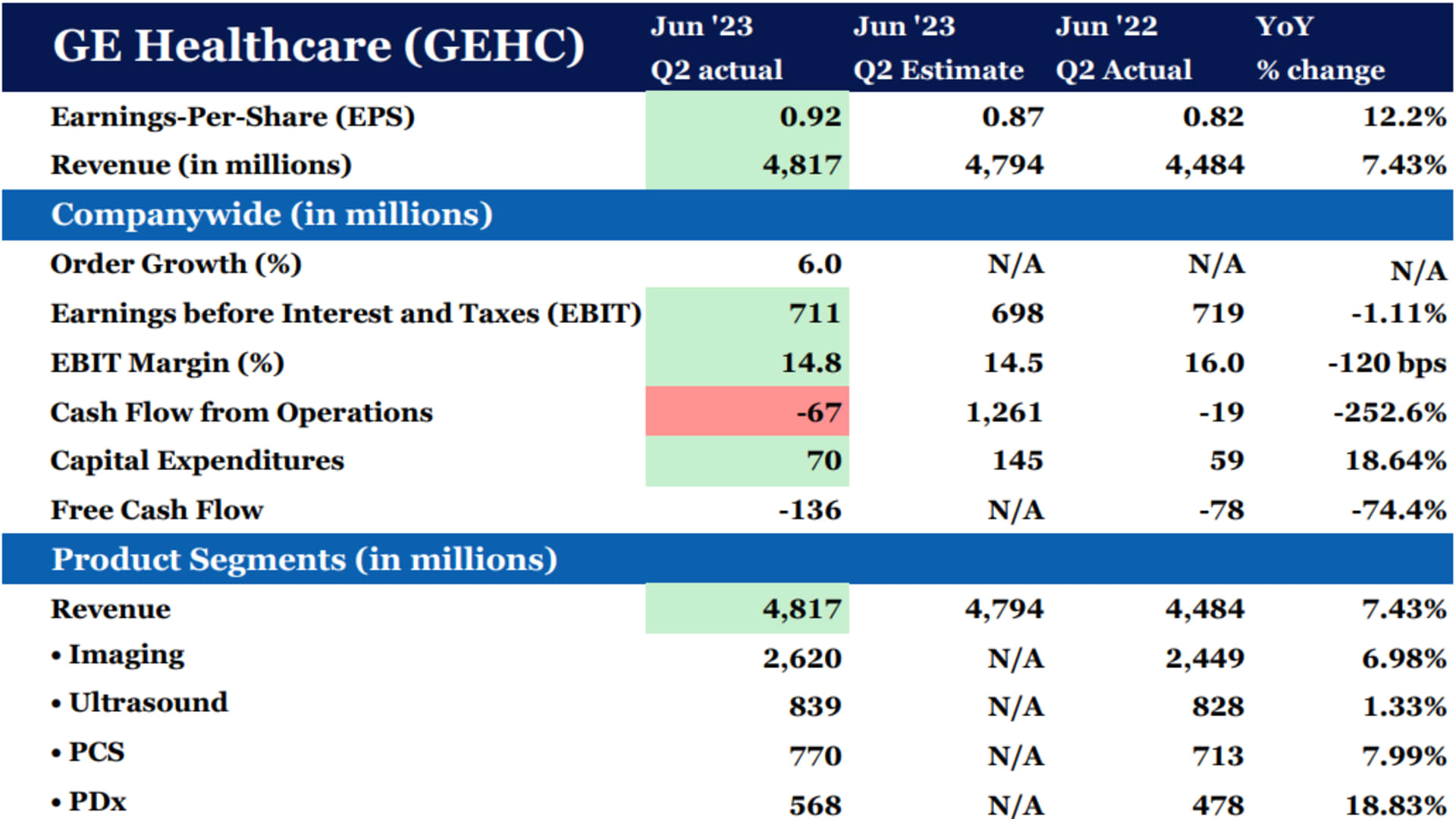

GE Healthcare Technologies ‘ (GEHC) second-quarter earnings beat and guidance raise are underappreciated by the market Tuesday, with the stock giving up early morning gains — but that only creates an opportunity to add to the Club’s nascent position. Total revenue for the three months ended June 30 rose more than 7% year-over-year, to $4.82 billion, beating analysts’ expectations of $4.79 billion, according to Refinitiv. Adjusted earnings-per-share (EPS) of 92 cents exceeded the Refinitiv estimate of 87 cents a share. Bottom line It was a solid quarter from this medical equipment giant — one that investors appear to be overlooking based on the selling pressure on the stock midday Tuesday. Shares were trading down around 0.85%, at just under $80 apiece. That small sell-off is misguided. The orders trend showed there is real momentum in the business, with a clear opportunity for more growth in the future as the company wins new business to support Alzheimer’s treatments. The company should be one of the big winners from recent advancements in the space, given it’s one of the few firms that offer a full suite of products and technological solutions to support patients with Alzheimer’s. With healthcare providers continuing to invest in equipment, leading to strong volumes across the board, and margins expected to improve in the back half of the year, GEHC is well-positioned. We first bought up a modest number of GE Healthcare shares in May, while patiently waiting for a retreat in the price. Now that we’ve seen shares pull back slightly, despite the beat and raise, we would look to add to our position once our trading restrictions allow. Second-quarter results Overall, GE Healthcare delivered solid second-quarter results. Total company orders increased 6%, representing an improvement from the 3% increase it saw last quarter. Investors tend to focus on orders because they’re indicative of customer demand. A mid-single-digit growth rate is a healthy one for this…

Read the full article here

Leave a Reply